The captured heart of Biden's LNG pause

Emissions metrics and financial sprints to favor the few and bewilder the many

In the name of climate change, President Biden announced a “temporary pause” on pending decisions for exports of liquefied natural gas in late January. The US is-or was- the global leader in LNG exports. LNG is almost entirely methane.

The White House characterized the decision as building on existing efforts to reduce methane emissions as part of the Global Methane Pledge and mobilization of financial support through Biden’s Methane Finance Sprint and the related Global Methane Hub.

All three, to the extent that they actually represent three separate activities, are supported by the same philanthropic entities- many of which are pictured below.

And so it appears that Biden has committed to significant changes in the US energy market in order to appease the likes of anti-gas billionaires such as Michael Bloomberg and Jeff Bezos, the latter of which is in cahoots with the State Department on a carbon offset scheme announced shortly after John Kerry announced stepping down from his political appointment as climate czar.

I do not know if a LNG pause is good US energy policy. However, the official reasoning for this policy change is rooted in the logic of emissions accounting and its legacy of ambiguous scientific concepts.

Emissions Metrics

There is a 30+ year saga around the use of emissions metrics in climate policy namely, global warming potentials (GWP), the core construct in emissions accounting for national and corporate inventories. A big part of the saga is a general befuddlement as to why the GWP concept won’t die because it does not work in the context of climate policy and causes serious errors on projected temperature changes.

The debate is extended and made more complex by the introduction of different metrics such as the global temperature potential (GTP)- a metric for which, component parts are used in documentation by the Global Methane Pledge and uncertainty ranges are reported by the IPCC as -50% to +75% for methane.

The reason the metrics persist (my focus being GWP) - and a big reason- is because powerful financial interests continually breathe life into it.

Consider for instance, that the US sent its top regulator of its financial derivatives market, Chairman of the Commodity Futures Trading Commission, to COP 28 in Dubai.

GWP is an index or a scaling factor to convert different greenhouse gases into carbon dioxide “equivalents” (often noted as, CO2eq). More technically, GWP is

the time-integrated [radiative forcing] due to a pulse emission of a given component, relative to a pulse emission of an equal mass of CO2

However, there is ambiguity as to what kinds of ‘global warming potential’ the GWP index is in reference. The IPCC explains,

A direct interpretation is that the GWP is an index of the total energy added to the climate system by a component in question relative to that of CO2. However, the GWP does not lead to equivalent temperature or other climate variables. Thus, the name ‘Global Warming Potential’ may be somewhat misleading, and ‘relative cumulative forcing index’ would be more appropriate.

The GWP concept is as old as the IPCC itself and it was modeled on the the Ozone Depleting Potentials (ODP) of the Montreal Protocol. GWP was more fully developed as a project between the IPCC and the OECD, and then revealed in the IPCC’s First Assessment Report (FAR,1990) with more details in a subsequent reports.

According to one notable scientist writing at this time:

It is difficult to see how GWPs could be used in any practical international treaty or in trading between greenhouse gases.

But used it is, widely.

According to the IPCC, emissions trading using ODP as a scaling factor had not been used much and had it been, it would have likely run into the same problems that are currently apparent with the use of GWP in greenhouse gas accounting.

Apples and Oranges

GWP calculations require a time period of interest. The most common time period considered is 100 years, denoted here as GWP-100. But, according to the IPCC,

There is no scientific argument for selecting 100 years compared with other choices (Fuglestvedt et al., 2003; Shine, 2009). The choice of time horizon is a value judgement because it depends on the relative weight assigned to effects at different times.

The time period chosen matters because not all gases behave like CO2 over time.

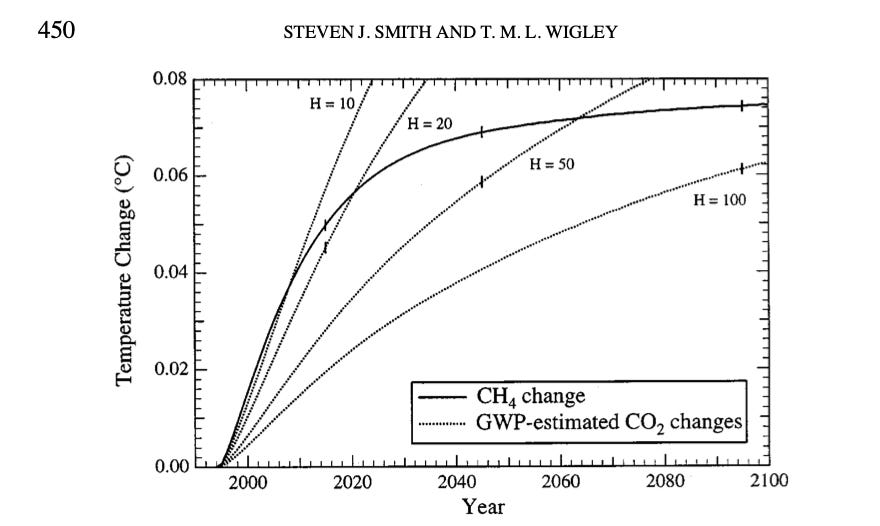

The graph below from Steven Smith and Tom Wigley in 2000, compares temperature projections using methane (CH4) directly and methane’s GWP- based equivalent on different time scales. Using a shorter time frame provides a more accurate GWP for methane.

As a result, aggregating gases using the GWP-100 concept and then using this aggregate to determine temperature changes produces large errors and muddies the already deeply uncertain translation of emissions into climate impacts. Smith and Wigley explain,

future temperature change, future sea-level rise, integrated temperature change, and integrated impacts can respond differently to the same relative change in emissions.

In other words, multi-gas GWP aggregates cannot be used as a stand-in for direct measures of the radiative forcing from individual gases.

While accountants are counting CO2eq, climate models are run using direct radiative forcing. It is meaningless to compare a GHG inventory calculated on GWP to climate model results commonly using IAM scenarios- which for all their other numerous problems, do produce measures of direct radiative forcings for individual gases.

It is standard accounting practice to calculate GWP-100 emission inventories and compare these to so-called 1.5oC aligned pathways developed using direct radiative forcing. The standard practice compares apples and oranges.

More recently, Wigley shows that this apples and oranges approach masks the significance of the emissions problem by hiding the time-varying effects relevant for discerning climate targets of interest. He finds that in order to meet the 1.5oC temperature target of the Paris Agreement net-zero needs to be met by 2036 (not 2050).

Wigley argues for a wholesale discard of GWP. One potential replacement is the use of direct radiative forcing for each gas.

In pursuit of regulation

Since Biden entered the White House, several recently proposed regulations would formally embed GWP-100 into Securities Exchange Commission (SEC) financial regulations and government procurement considerations. Such regulations effectively move the GWP saga from the political theatre of international climate change policy to formal accounting practices for one of the world’s most significant financial markets.

Late last year, the CFTC proposed rules for a voluntary carbon credit derivatives market. The system is founded on the GWP-100 aggregate because this is the standard for calculating carbon credits and offsets.

While, I have no idea if the LNG pause has led to a change in market carbon prices, I note that there was a rally in the voluntary carbon market following Biden’s announcement on January 26.

The proposed derivative rule linked its standards to an organization with Mark Carney on the board. This was all around the time TCFD announced it had fulfilled its mandate and was closing up shop, and Bloomberg’s trusty sidekicks former SEC chair Mary Shapiro and corporate sustainability lead Curtis Ravenel joined Carney as advisers to the disclosure platform unicorn, Watershed.

There are many activities that tie together these successful business entrepreneurs and Watershed’s investors. But the one core construct that they all rely on is GWP-100.

This is because the “the basis of climate accounting” is the GHG Protocol, which requires use of GWP-100. As well, TCFD- itself the current foundation for contemporary climate risk disclosure practices- anchored its disclosure recommendations on the GHG protocol, as you can see below.

Concurrent with the passage of the Kyoto Protocol, the World Resources Institute (WRI) and the business coalition, World Business Council for Sustainable Development (WBCSD), created the GHG Protocol.

It’s worth recalling a bit of political history here. A lead negotiator of Kyoto was the then Vice President Al Gore. WRI was founded and led by Gus Speth, a former political adviser to Clinton and, at the time, head of the UNDP. WRI led the development of a carbon offset market and Gore went on to a career in ESG investing.

Then, concurrent with the passage of the Paris Agreement came the development of the Science Based Target initiative. SBTi requires use of the GHG Protocol and then compares the GWP-100 multi gas aggregate to emission scenarios aligned with a 1.5oC target using individual gases direct radiative forcings. Apples and oranges.

SBTi was developed by

WRI

World Wildlife Fund

CDP

which “run[s] the global disclosure system” for sustainability, (emphasis added)

UN Global Compact (an NGO)

corporations gain access to political support after a commitment to several UN principles and a fee. Its board chairman is the UN Secretary General Antonio Guterres.

We Mean Business- a coalition of advocacy groups and other business coalitions, requires its members to commit to SBTi.

We Mean Business includes

WBCSD, and CDP

Ceres

business and investment coalition

BSR

“a sustainable business network and consultancy”

An executive group run out of the University of Cambridge

Climate Group

organizes the annual NYC Climate Week festival

The B Team

corporate advocacy group

That’s a whole lot of coalitions of coalitions all invested in a bad concept anchored into scientific reporting and international policy.

The relationship looks like this:

Accountability, please

Some US legislators are skeptical about the extent of coalition building and agreements among interests in carbon trading and climate risk disclosures arguing that it presents antitrust violations.

Most recently, US Representatives held a hearing to examine why the White House would require the government procurement process to use SBTi, which they note also receives funding from Arabella Advisors.

The White House representative testifying explained SBTi was used because that is the authoritative standard. This a self referential statement. It’s the existing authoritative standard because it is created, used, and advocated for by all the same interests in the development of a market that they lead.

When GWP appeared in the FAR Report (FAR), it was introduced “to illustrate the difficulties inherent in the concept…”

Nearly 20 years later, Keith Shine, a climate scientist close to the subject, reflected on the persistent use of GWP despite its problems, predictions that it will die, and scientific efforts to offer better options:

Did something go wrong here? How did “a simple approach” which was “adopted . . . to illustrate . . . difficulties” become established in a major piece of environmental legislation, where it had the potential to influence big investment and policy decisions?

…has there been what might be termed an “inadvertent consensus”, so that the IPCC and policymakers have each perceived that the other was content with the concept and didn’t apply pressure to fully assess alternatives?

If policymakers are hell bent upon using GWP then scientists would build careers on researching it. Writing in 1999 as part of her doctoral studies, Tora Skodvin, now a professor of political science at University of Oslo, explained:

Most scientists, and not only natural scientists, have experienced that when policy-makers really need a specific kind of knowledge that scientists are able to provide, they very soon lose interest in the caveats expressed in the fine print.

And so, today, we see things like scientists defending the continued use of GWP on political terms. For instance, one recent defense of GWP in ERL:

Whether or not we agree with the ‘inadvertent consensus’ that the simple GWP metric has enjoyed since 1990 (Shine 2009 [as above]), the fact is that hard-wrung policy architectures are now in place. The theoretical benefits of any GWP-alternative must be weighed against the political capital required to overhaul existing policies and targets.

The authors of this political defense of GWP provide climate analytic consulting using GWP-100 in their methodology. Of course, the authors declared no conflicts of interest.

As framed, Biden based the entirety of this decision with national and international significance on a complex system of conflicts of interest holding together calculative practices not fit for purpose.

GWP-100...SBTi....Watershed....TCFD...WRI...WBCSD....WWF....Ceres....SEC...CFTC

It's the self-licking ice cream cone, Doc.

Please help me out here, Dr. Weinkle. As I read your figure from Wigley, et al, if methane emissions were to suddenly drop to zero, the net temperature change would be about 0.75 C? Is that correct? So, we are willing to eliminate an industry that generates $122 billion in revenues, in order to prevent temperatures from rising an amount that is undetectable, to meet a global standard (GWP) that lacks precise meaning or measurement?

Please tell me I'm wrong, someone, anyone...because if my interpretation is correct, this is insanity.