"Housing policy is disaster mitigation policy"

Home prices are softening and climate change has nothing to do with it

In recent months, home values have softened in formerly hot real estate markets. The news has been awash with that there are now more sellers than buyers.

A story in Bloomberg attributed the downturn to climate change induced rises in homeowners insurance.

However, most following the 60 year debate about homeowners insurance costs are well aware that the trend in costs are a result of exposure and broader socioeconomic trends.

According to Swiss Re:

Losses are primarily driven by socioeconomic factors. The main driver keeping insured losses on a steep upward trajectory is rising exposure values as a result of economic growth and expanding populations, often in regions susceptible to severe weather conditions

On May 1, the Senate Committee on Housing, Banking and Urban Affairs took up the insurance cost issue.

Chairman Tim Scott (R): opened the hearing blaming the lack of coverage on state regulatory environments:

[Insurance markets] should be based on sound actuarial and underwriting principles, not artificial mandates that distort prices and ultimately hurt consumers.

Okay. But rate suppression is aimed at keeping the insurance affordable. So, while constrained pricing leads to insurers leaving markets it doesn’t address the affordability issue.

Ranking Member Warren (D) lamented President Trump’s various activities. In her opening remarks Senator Warren (D) redirected1 the conversation to Trump’s tariffs:

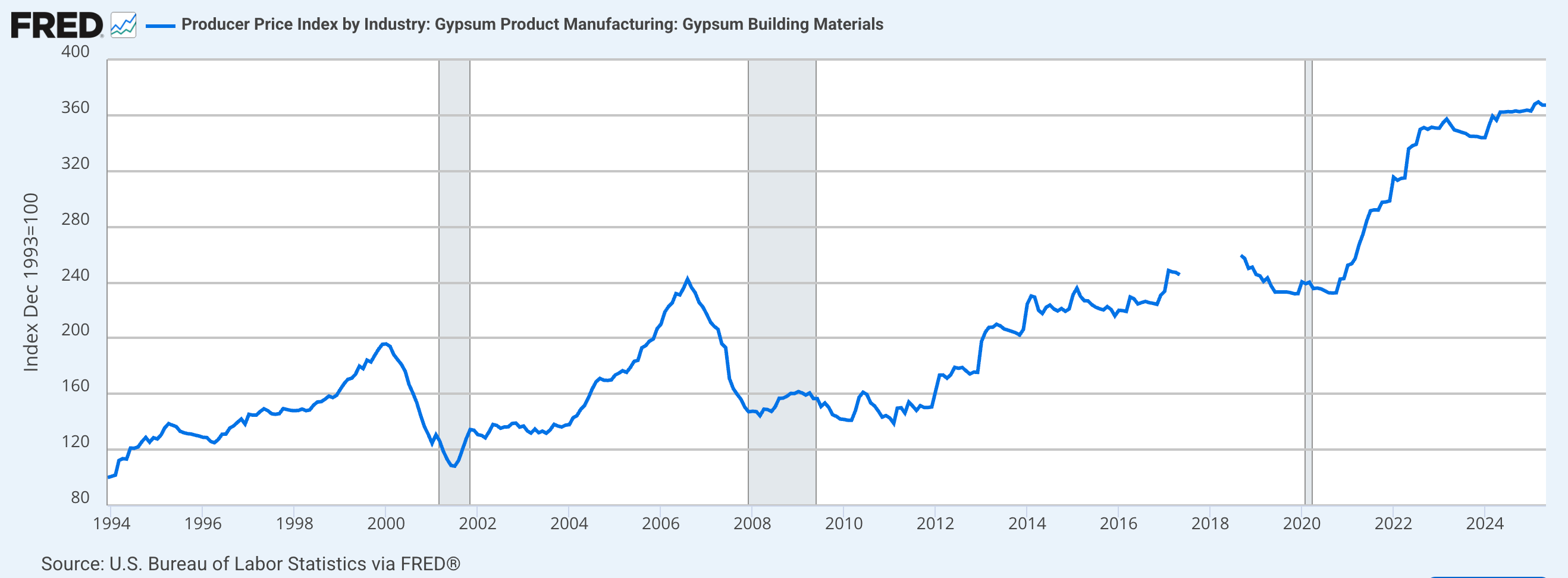

These tariffs will make just about everything needed to rebuild and repair houses more expensive: aluminum, HVAC systems, appliances, gypsum, and on and on.

Okay. But the increasing price of gypsum and other building materials began well before Liberation Day.

Swiss Re provides the following explanation about the cost of rebuilding:

Net incurred losses of homeowners insurers’ nationwide rose at a compound annual growth rate (CAGR) of 8% between 2018 and 2024. The key economic driver was construction costs, up around 40% between 2020 and 2022. This was far in excess of the consumer price index, which pushed up claim costs for insurers

About half way through the Senate hearing (~57:03), Senator Warren states:

We cannot fix our housing crisis without fixing our skyrocketing insurance costs.

I think this is wrong and it’s been wrong for a long time.

Looking in the opposite direction is more fruitful: We cannot fix the problem of insurance costs without fixing the problem of housing.

The reason for this is so is that what goes on in the housing market is a reflection of and contributor to the overall economy of states and nations, and household wealth. Damage to housing is the underlying cause of loss and hence, insurance costs. There are a lot of policy levers in housing: production, design, construction, lot size, zoning, mortgage structures, and so on. Urban infrastructure that supports disaster mitigation also supports housing.

In contrast, there are few levers in insurance and seemingly not much political appetite for massaging insurance markets and practices.

Giving testimony at the hearing, a representative of the Insurance Institute for Business and Home Safety argued that “housing policy is disaster mitigation policy.”

Indeed.

Policymakers should put more effort on addressing housing affordability while balancing it with urban infrastructure improvements as an oblique means of addressing insurance problems.

Rising insurance costs, of course, puts pressure on homeowners. It is a cost that increases steadily and is susceptible to spikes. However, it is inappropriate to cast the current state of the housing market as an insurance problem and even more absurd to call it a climate change problem.

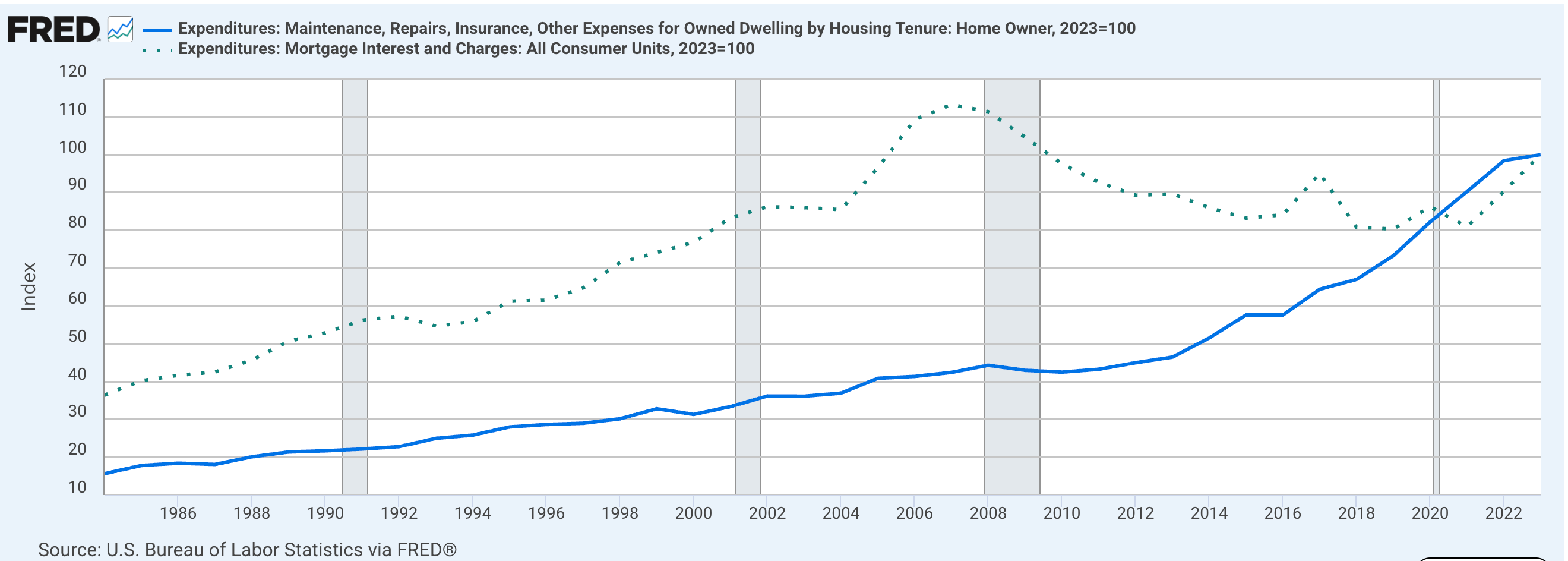

Swiss Re puts the cost of homeowners insurance at about 9% of the sum of expenses for new mortgages (principal and interest), insurance and property tax. They further note that financing costs for new mortgages nearly doubled between 2020 and 2023.

Since the global financial crisis until very recent years, the steady increase in insurance costs coincided with low mortgage interest rates.

The chart below shows that the while homeowners saw a decline in mortgage interest costs, insurance costs- along with maintenance and repairs, continued to increase.2 Mortgage costs spiked in 2022 while insurance costs continued its ascent.

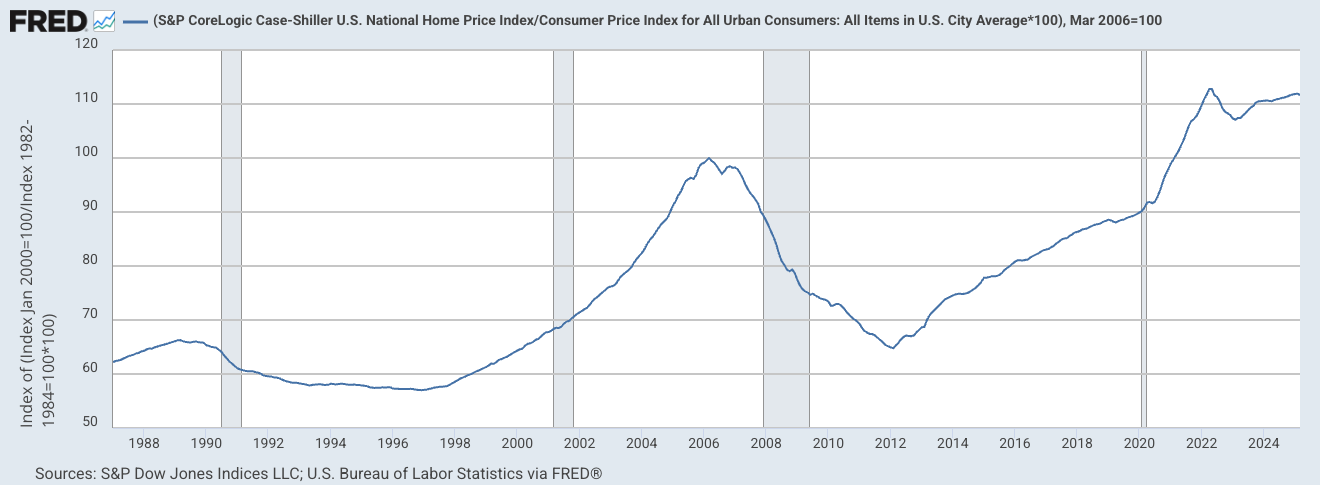

Home prices have steadily increased since 2012 and rapidly so after 2020.

Thus, the increased cost of insurance is added on to what are already very expensive homes and relatively costly mortgages. This is not a climate issue.

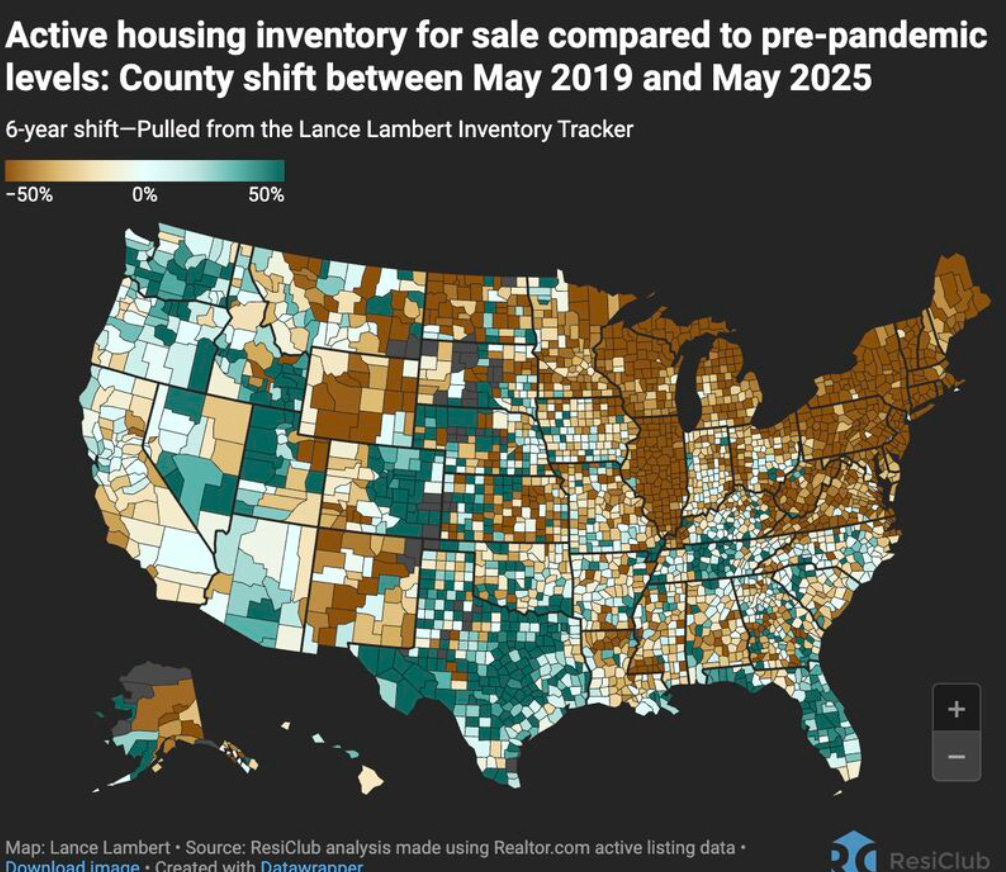

The current trend of falling home prices is a broader trend than just in Florida.

Lance Lambert, head of ResiClub, has a series of popular graphics showing the shifting inventory accompanied by a reversal of price trends.

Common reasons I’ve seen cited as cause of this shift is company claw back of work-from-home policies that became popular during the pandemic. Another reason is the skyrocketing prices of housing in the Sun Belt (including insurance cost spikes) making it less attractive than years prior.

The slowdown could have become more apparent earlier, however, Lambert also points to the role of large homebuilders have had in masking the impact by squeezing their own margins through homeowner financing options in order to keep new builds selling.

Lennar is mentioned as the most aggressive pursuer of this strategy. As it happens, Lennar is the largest homebuilder in Florida.

Builders are now turning to price cuts to keep selling houses.

A result of this, according to Lambert, those who bought into a neighborhood first are now underwater,

sometimes north of 25%. It is sad because if that [sic] had to move, they can't sell their homes because Lennar/DR is offering a new home, at 20% less, with a mortgage rate 150bps less than market too.

Hold that thought.

In the next post, I’ll take up the media headlines about climate change, insurance, and foreclosures.

She also pointed to climate change and uncertainty about FEMA

Climate change is such a convenient and lazy excuse to avoid tackling the actual root causes of many problems.