A Very Good Number

Florida's Citizens Property Insurance is at a record low policy count. Does that mean anything?

I’ve followed along with news about the hurricane (windstorm) insurance market in Florida for the better part of 20 years. Sometimes, I pay close attention, sometimes less.

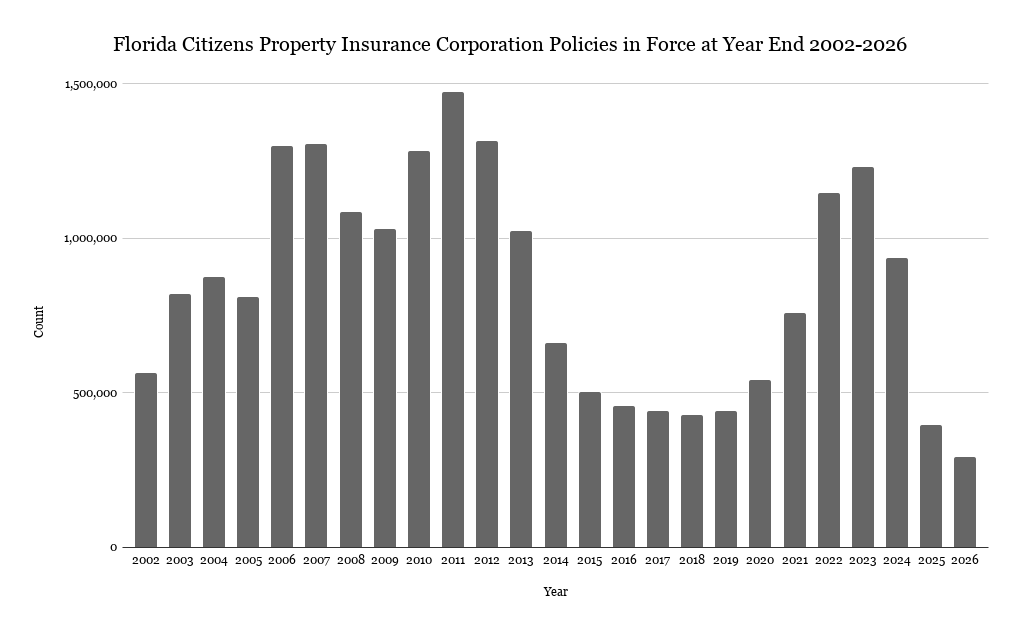

It is notable that the Florida Citizens Property Insurance Corporation (CPIC) is at its lowest count of policies in force since its creation in 2002.

The May count of 293,772 is far below the roughly 400,000 level CPIC identifies as the “residual market level.” Peak December policy count occurred in 2011 with 1,472,391.1 The more recent peak occurred in 2023 with 1,228,718 policies.

Acknowledging the milestone and making sense of the data series is important for understanding broader debates about catastrophe insurance in which CPIC is usually used as the poster child of ill repute.

The Florida Citizens Property Insurance Corporation (CPIC) is the state’s residual market for property and windstorm insurance. Its guiding legislation establishes that it is intended to provide “affordable” property insurance:

The Legislature intends, therefore, that affordable property insurance be provided and that it continue to be provided, as long as necessary, through Citizens Property Insurance Corporation, a government entity that is an integral part of the state, and that is not a private insurance company.

The Florida legislature created the CPIC in 2002 by merging the Florida Windstorm Underwriting Association (FWUA) with the Residential Property and Casualty Joint Underwriting Association (JUA).

The FWUA dates back to 1970 during the era of state created Beach and FAIR plans. The JUA was created in 1992 to help stabilize the state insurance market after Hurricane Andrew. Merging the two provided the state with administrative efficiencies.

Shortly after CPIC was created, Florida was impacted by 7 hurricanes landfalls during the 2004 and 2005 seasons. These large losses, subsequent market tightening, and catastrophe model changes created affordability problems and in turn, instability in the market.

In 2007, the Florida legislature responded with changes to CPIC rates and eligibility that enabled it to grow until its peak in 2011. The legislative response also aligns with the global financial crisis.

The CPIC depopulation effort that followed was aided by fortunate timing with a prolonged lull in US major category hurricane landfalls.

Since 2017, Florida has benefited from a consistent pattern of strong hurricanes missing the state’s most concentrated urban hubs:2

Hurricane Irma (2017), Cat 3 Landfall, Marco Island; ~$23B in US+Caribbean

Hurricane Michael (2018), Cat 5 LF, a rural/ not so populated part of the panhandle; $10B

Hurricane Ian (2022), Cat 4 LF, Cayo Costa/Cape Coral; ~$53B

Hurricane Idalia (2023), Cat 4 LF, rural Big Bend area; $1.75B

Hurricane Helene (2024), Cat 4 LF, rural Big Bend area; $16B

Hurricane Milton (2024), Cat 3 LF, Siesta Kay/Sarasota; $25B

The notable on the list is Ian which could have been a lot worse had landfall centered on Tampa.

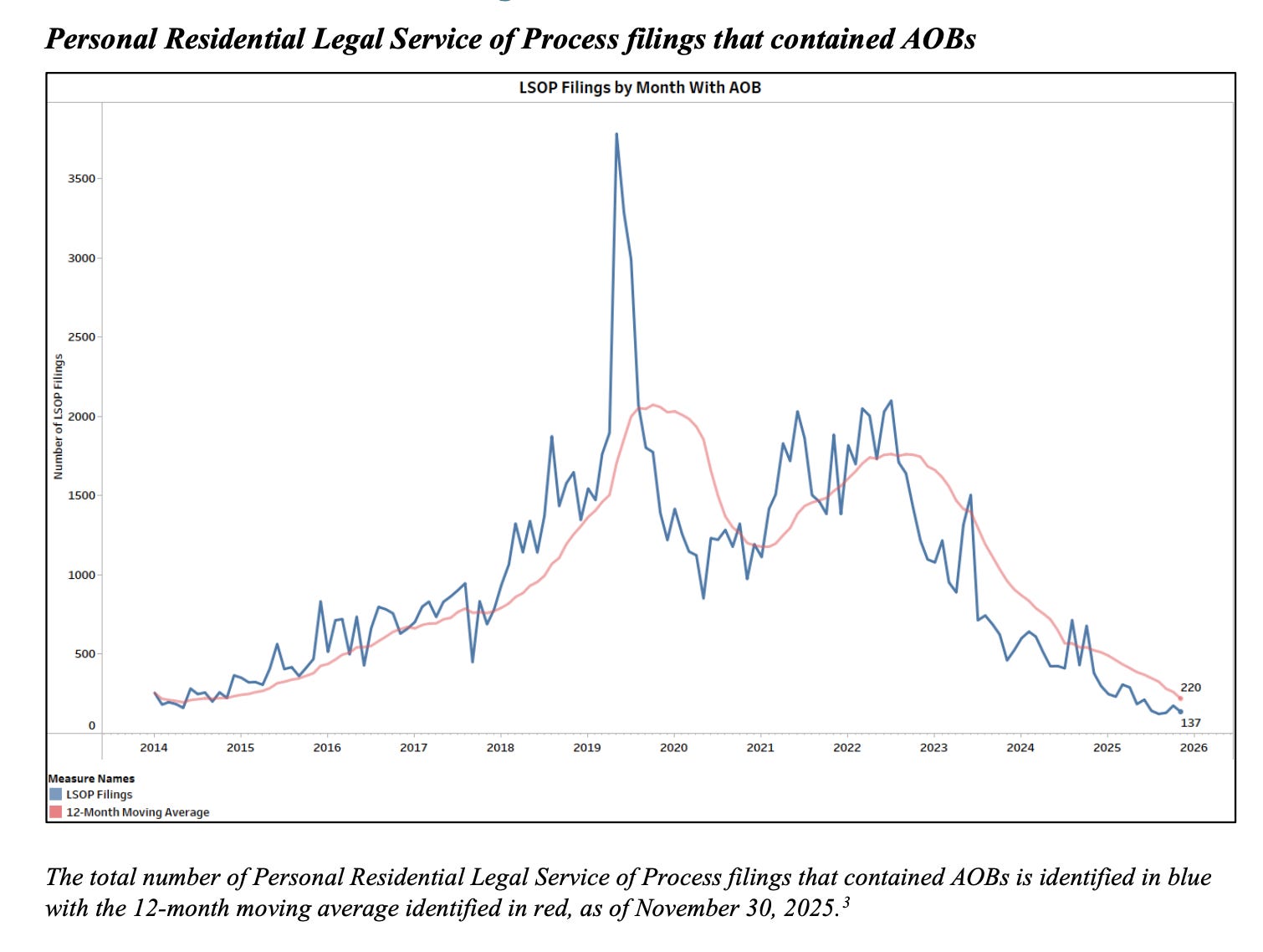

The grumble about Irma and Ian were their long tail of claims. Litigation costs and assignment of benefits (AOB) abuse amplified the loss experience beyond the storms’ physical damage.

About a month before Ian’s landfall in September, III pushed a press release reporting that,

Florida is the site of 79% of all homeowners insurance lawsuits over claims filed nationwide while Florida’s homeowners insurers receive only 9% of all U.S. homeowners property insurance claims.

Legislation to effectively end the AOB problem passed in December 2022 and thus, did not apply to Ian losses. The graph below from the FL Office of Insurance Regulation (FLOIR) January 2026 report shows the AOB pattern including its recent decline. The big spike in 2019 is, I believe, Irma’s long tail of AOB issues.

The rapid decline in CPIC policy count since 2023 is generally attributed to legislative changes curbing insurance litigation activity thereby improving overall market participation interest.

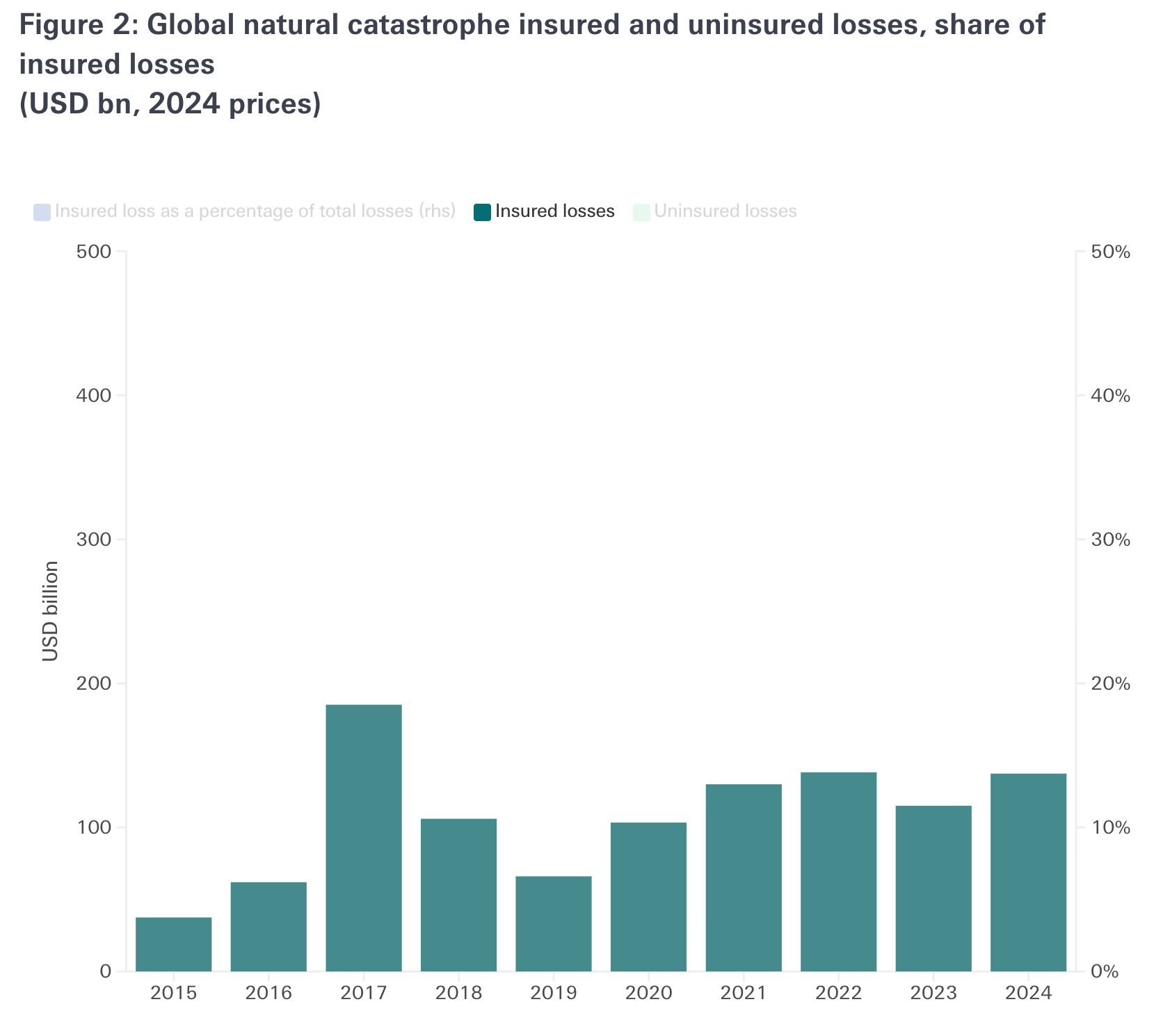

The chart below is from Swiss Re showing the large loss year of 2017 driven strongly by hurricanes Harvey, Irma, and Maria. Despite the 2017 losses, CPIC policies stayed fairly stable through 2019.

Thus, the increases in CPIC policies between 2020 and 2023, had less to do with catastrophe losses per se, but compounding factors around those losses: the litigation/AOB issues, inflation was especially high then, too.

In addition, between 2019 and 2023/2024, US reinsurance Rate on Line increased by 83%. Other metrics around the web suggest reinsurance costs fully doubled. Reinsurers increased their attachment points pushing primaries to retain more risk culminating in the “Great Realignment” of 2023.

Much of this was done under a public facing narrative of climate change. However, Howden, which originated the catch phrase, situated it into a broader gist of political and economic instability,

The effects of COVID – huge fiscal and monetary stimulus, supply constraints and high debt burdens – have collided with the devastating fallout from Russia’s invasion of Ukraine to bring about a great realignment, characterised by structurally higher inflation, rising interest rates, heightened security threats and accelerated deglobalisation.

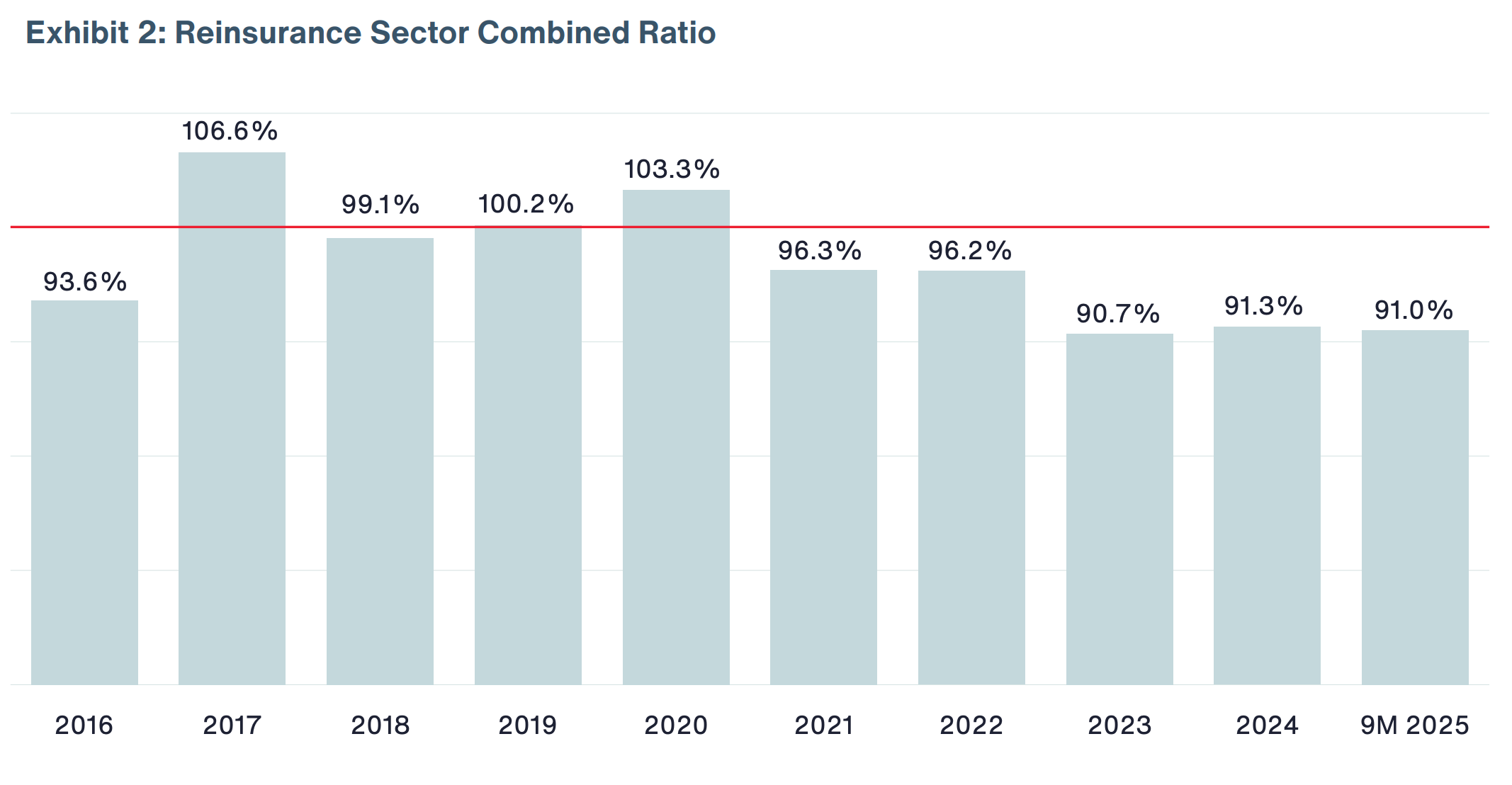

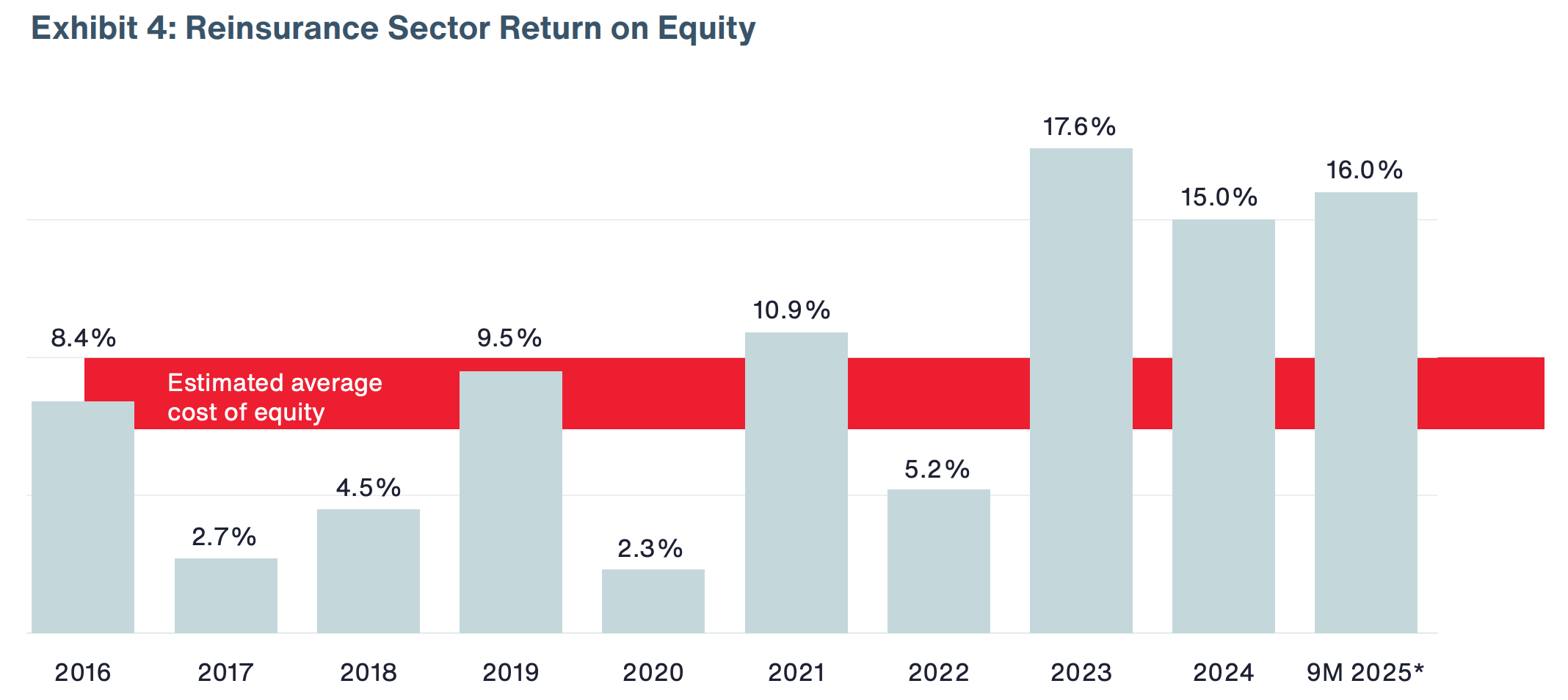

The marketing and general sense of trepidation was accompanied by very profitable years. The below graphs come from an Aon January 2026 report.

This year, reinsurance pricing is on the way down while terms are “mostly holding” meaning that the great realignment persists.

Florida’s property insurance market is dominated by the reinsurance sector. FLOIR explains,

Florida’s domestic property insurance industry is especially reliant on reinsurance to finance the payment of catastrophe losses and is sensitive to hardening reinsurance market conditions.

That’s a bit of an understatement. According to AM Best,

The top 10 active Florida composite companies exhibited an average ceded reinsurance leverage of 562% in 2025 compared with 55% for the U.S. personal property composite average.

What this means is that Florida insurers are thinly capitalized relative to standard practice. What a Florida insurer holds in capital is very small compared to the total risk it is originating.

As a result, Florida’s primary market is more like a conduit for the reinsurance market than it is a traditional layer in risk transfer.

It also means that a Florida domestic doesn't fail in the classic sense of mispricing risk and becoming insolvent. It fails because its reinsurance tower collapses by way of inaccessible reinsurance. Well, that and overzealous litigation.

Between 2019 and 2023, over ten Florida P&C providers failed.3 But, as I understand it, none of these failed in a traditional way. They failed from the litigation burden and/or an inability to secure reinsurance.

In 2022, the Florida legislature created new reinsurance mechanisms to complement the existing Florida Hurricane Catastrophe Fund. The Reinsurance to Assist Policyholders (RAP) a free (ahem), taxpayer supported reinsurance layer just below the FHCF. It still exists but has been significantly wound down from its original $2 billion.

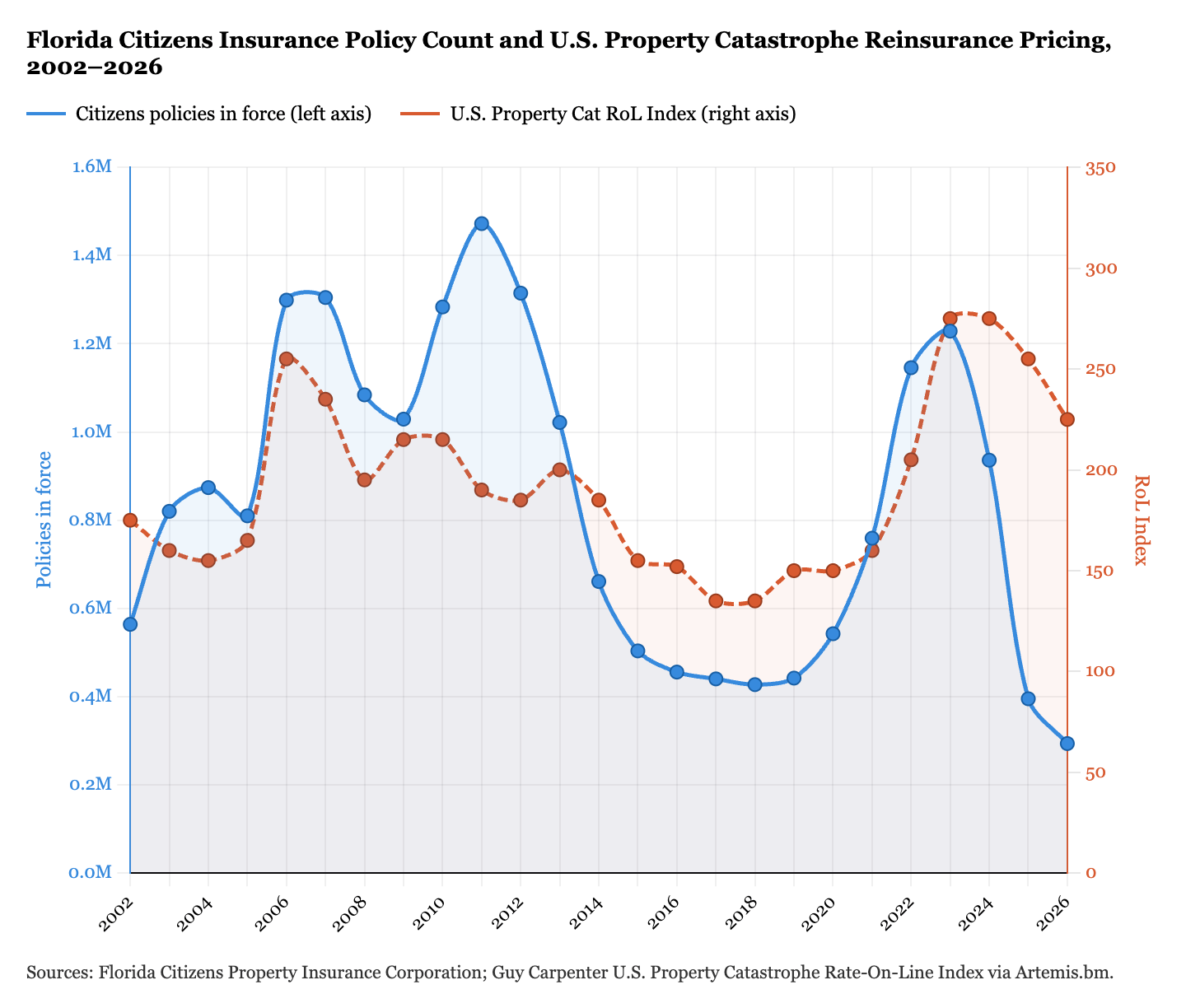

The chart below shows the relationship between CPIC policy count and the Guy Carpenter US reinsurance Rate on Line (ROL) Index. The two do not mirror each other exactly but there is a general similarity.

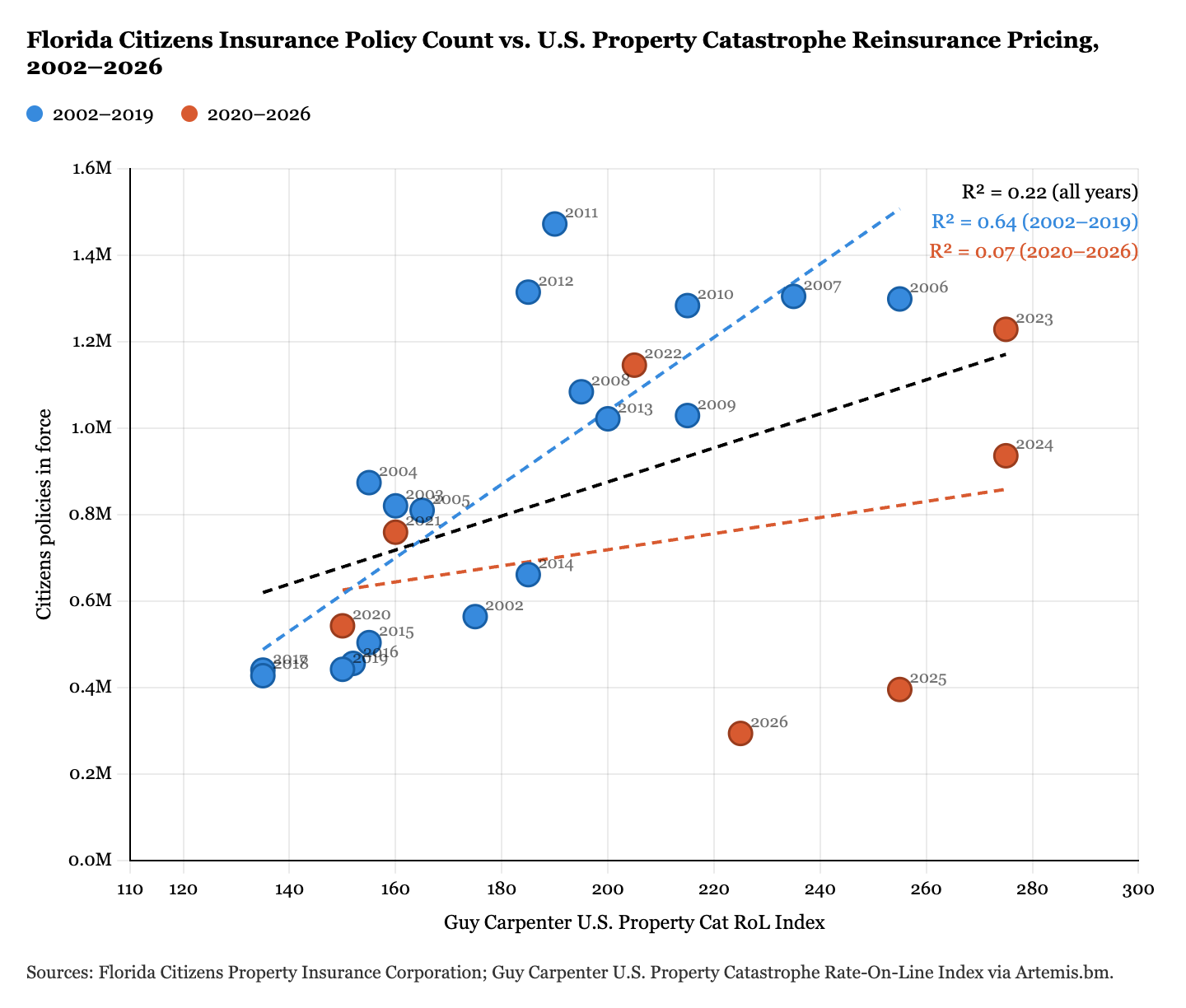

The scatter plot below measures how much of the variation in Citizens policy counts can be explained by reinsurance pricing. The correlation between the two data series is 0.22 over the entire time period. However, when analyzed separately, the correlation for 2002-2019 is 0.64, while the correlation from 2020-2026 is very low, 0.07.

The lack of correlation in the most recent period likely reflects the degree to which the litigation problem and its reform influenced CPIC policy count.

The question then is if the current CPIC low policy count is simply a return to the longer depopulation trend that occurred alongside low hurricane losses and a soft market, or if it represents something more structurally different in a primary market functioning as a pass-through4 to a reinsurance market that has remade its terms so as to be less accessible.

I’ve never been one to bag on CPIC and the state’s wrangling of the hurricane risk problem. There has been tremendous ingenuity in Florida’s handling of large cat risk.

It seems to me however, that CPIC’s low policy count is less of a great success story and more of a transformation of the story’s character from a slow moving, very visible situation, to a potentially rapid and structurally opaque one.

My final musing…

Large losses in Florida are a real concern but they are only one piece of the story about how losses play out in their eventual effect on policyholder costs which create affordability/availability tensions and thus, instability.

Macro level trends provide the context for how a loss event will be felt through the system. Would Florida’s situation post 2004/2005 been so challenging had it not been ground zero for the mortgage crash of the Global Financial Crisis? Maybe not.

Artemis cited Swiss Re in providing the following:

If the long-term growth trend for insured losses globally continues at its 5-7% annual pace, Swiss Re warns that insured losses could reach US $186 billion by 2030 globally, up from US $107 billion in 2025.

That 7% undoubtedly reflects exposure trends.

The responsible reaction is not “oh my, that’s a big number let me fiddle with my hurricane tracks and warming scenarios.” Instead, the right what-if questions to ask are about the bigger picture:

What happens when big losses- in Florida or elsewhere- occur

during a war,

a recession,

declining population,

supply chain disruptions,

energy shortages,

different flavors of political ineptitude, or

if Florida loses its cruise ship industry because Miami Beach dropped the ball on securing the fuel depot from the fantastical elite NIMBY’s on Fisher Island.

For all I know, these discussions do take place in private boardrooms in Tallahassee and around the world. But I don’t see it coming through in public debate. It should.

I invite critique on this. It is likely to become part of a longer academic paper about the unproductive way the homeowners insurance problem is framed.

This value is larger than a 1998 value I have in my records of 1,402,576, predating the creation of CPIC. I’m not sure if that value is the FWUA+JUA or just the JUA.

loss values from Aon and MunichRe reports

Google Gemini reports that these were: United Property & Casualty Insurance (UPC): Went into liquidation in early 2023; FedNat Insurance Company: Placed into receivership for liquidation in late 2022; Southern Fidelity Insurance Company: Liquidated in 2022 after exhausting its catastrophe reinsurance; Weston Property & Casualty Insurance: Entered liquidation in 2022; Avatar Property & Casualty Insurance: Went into receivership in 2022; Lighthouse Property Insurance Company: Ordered into liquidation in 2022; St. Johns Insurance Company: Placed into receivership in 2022; Gulfstream Property and Casualty: Consented to a receivership order in 2021; American Capital Assurance Corporation (ACAC): Ordered into liquidation in 2021; Florida Specialty Insurance Company: Liquidated in late 2019; Windhaven Insurance Company: Liquidated in January 2020; Windhaven National Insurance Company: Liquidated in March 2020.

To be sure, people have said for a long time that the FL domestics are undercapitalized.